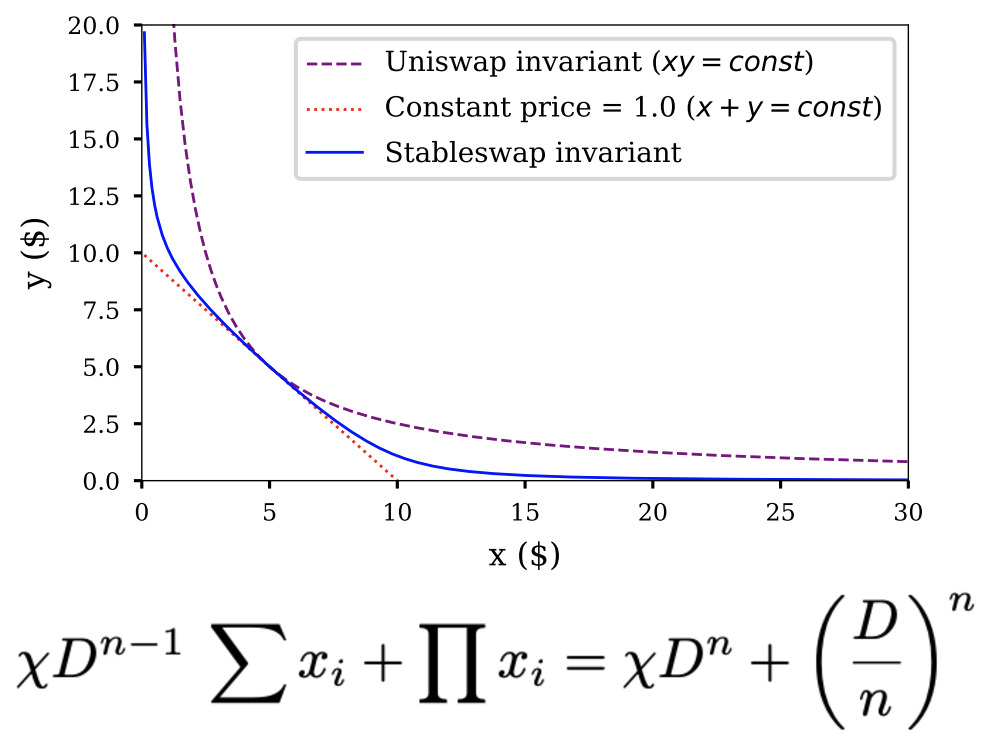

How StableSwap reduces slippage

StableSwap solves the liquidity inefficiency that plagues constant product models like Uniswap V2 when handling pegged assets. Traditional automated market makers (AMMs) spread liquidity evenly across all price ranges, which works well for volatile pairs but creates high slippage for stablecoins that trade near a 1:1 ratio. StableSwap changes this by blending two mathematical invariants: the constant product formula ($x \times y = k$) and the constant sum formula ($x + y = C$). This hybrid approach allows the pool to behave like a constant sum swap when prices are close to parity, effectively offering infinite liquidity at the peg and near-zero slippage. As prices drift further from the peg, the curve gradually transitions to the constant product model, ensuring the pool remains solvent and liquid even during significant deviations.

This mathematical blending is not just a theoretical improvement; it is the core mechanism that allows platforms like Curve Finance to offer deep liquidity with minimal price impact. By concentrating liquidity density near the 1:1 ratio, StableSwap pools maintain peg stability far more efficiently than traditional AMMs. This design choice means that traders moving large volumes of stablecoins do not suffer the steep price penalties they would encounter on a standard constant product pool.

The visual representation of this curve illustrates the trade-off clearly. Near the center, the curve is nearly linear, mimicking a direct exchange. As you move away from the center, it bends into the hyperbolic shape of a constant product AMM. This ensures that the pool can handle both small, high-frequency stablecoin swaps and larger, less frequent arbitrage trades without breaking the peg or running out of liquidity.

Comparing StableSwap and Constant Product AMMs

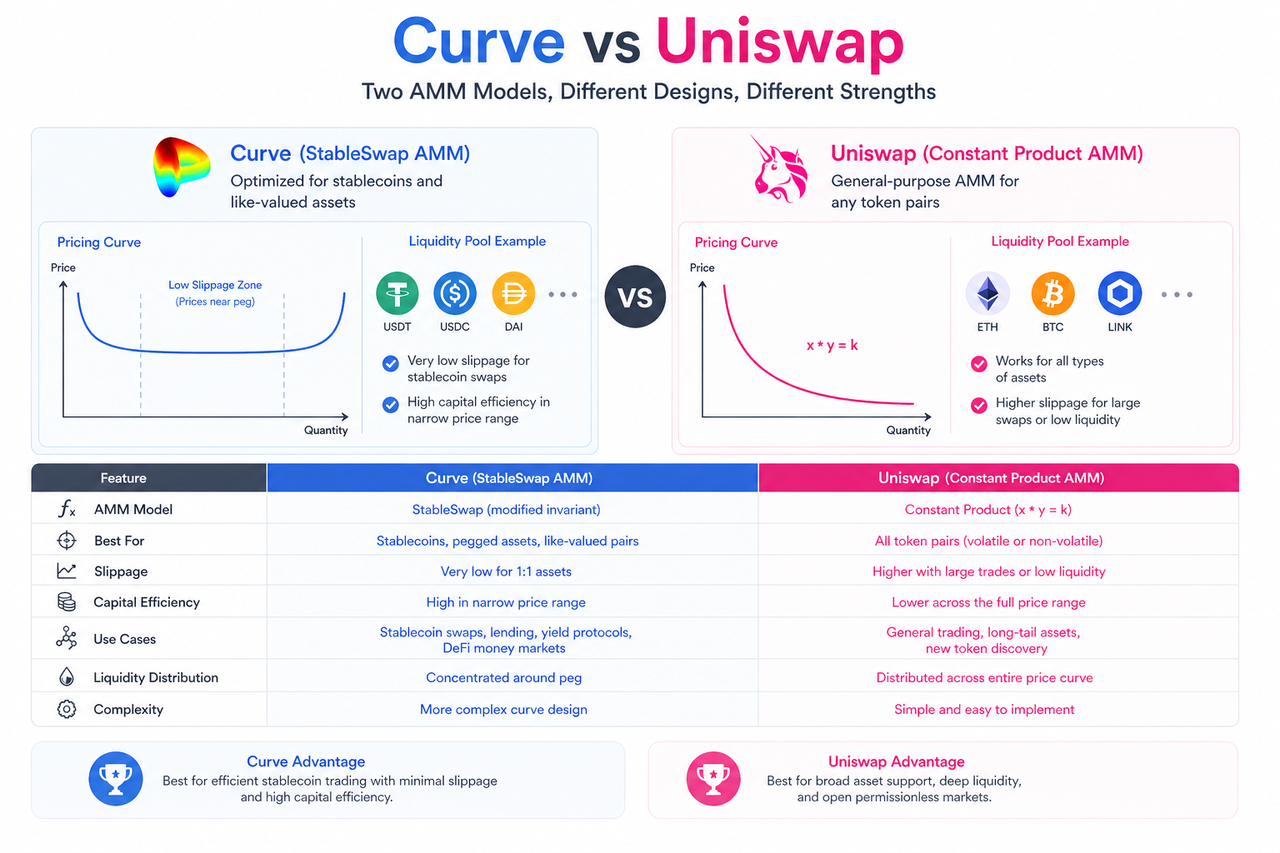

Choosing between StableSwap and traditional Constant Product AMMs depends on how much slippage you can tolerate and how efficiently you want to use capital. StableSwap models, such as those used by PancakeSwap and KokonutSwap, are engineered specifically for stablecoin pairs. They maintain concentrated liquidity around a 1:1 price range, which drastically reduces the slippage cost for large trades compared to the standard $x \cdot y = k$ invariant.

The primary advantage of StableSwap is capital efficiency. Because the algorithm assumes prices will remain pegged, it does not need to hold the same depth of liquidity as a Constant Product AMM to absorb large orders. This results in lower slippage for traders and higher yields for liquidity providers. However, this efficiency comes with a trade-off: StableSwap protocols are less flexible. They perform poorly with volatile assets, where the Constant Product model’s ability to adjust prices dynamically is a feature, not a bug.

Gas costs also differ between the two. While both models are optimized for blockchain execution, newer StableSwap algorithms like Wombat use closed-form solutions that can be more gas-efficient than older implementations, though this varies by specific protocol architecture.

For traders moving large amounts of USDC or USDT, StableSwap is the clear choice. The difference in slippage can mean hundreds of dollars saved on a single transaction. Conversely, if you are trading against volatile assets or providing liquidity for pairs that frequently deviate from peg, the Constant Product model remains the industry standard.

Tradeoffs in capital efficiency

While StableSwap models like Curve’s StableSwapNG offer superior rates for pegged assets, they introduce distinct tradeoffs that traders and liquidity providers must weigh against constant product AMMs. The primary friction points involve computational complexity, gas costs, and the hidden risks that emerge when pegs break.

The core limitation of StableSwap lies in its invariant formula. Unlike the simple constant product formula ($x \cdot y = k$) used by Uniswap, StableSwap employs a more complex hybrid invariant that blends constant product and constant sum mechanics. This mathematical sophistication allows for minimal slippage on stable pairs, but it requires significantly more computational resources to execute. As noted by technical analyses of the Curve AMM algorithm, these complex calculations result in higher gas costs per transaction compared to simpler AMM designs. For high-frequency traders or small retail swaps, these elevated costs can erode the benefits of lower slippage.

Liquidity providers face a different set of risks. StableSwap pools are designed to minimize impermanent loss (IL) when assets remain tightly pegged. However, this protection is conditional. If the peg breaks and the assets diverge in value, the pool’s behavior shifts toward that of a constant product AMM, exposing LPs to significant IL. This risk is particularly acute in volatile markets or during macroeconomic shocks that cause stablecoins to de-peg. Unlike constant product AMMs, which are inherently more robust to price divergence, StableSwap pools can suffer sharp value drops for LPs when stability fails.

Additionally, the complexity of StableSwap contracts can introduce additional security considerations. The intricate math and multiple parameter configurations increase the attack surface for smart contract vulnerabilities. While established protocols like Curve have undergone extensive audits, the general rule of thumb is that simpler AMM structures are easier to verify and less prone to edge-case exploits. For protocols prioritizing maximum capital efficiency with stable assets, the tradeoff is clear: you gain tighter spreads and lower slippage, but you pay higher gas fees and accept greater complexity risk.

Best StableSwap protocols in 2026

The StableSwap algorithm remains the standard for trading pegged assets, prioritizing capital efficiency over the wide price swings seen in traditional automated market makers. By adjusting the invariant curve to flatten near parity, these protocols minimize slippage for assets like USDC, USDT, and DAI, making them the preferred infrastructure for large stablecoin swaps and yield farming.

Curve Finance

Curve Finance continues to dominate the stablecoin trading landscape, holding the largest share of total value locked in StableSwap pools. Its core innovation lies in the "StableSwap invariant," which allows for near-zero slippage on pegged assets while maintaining liquidity depth. Curve’s recent upgrades have further optimized its fee structure and governance mechanisms, solidifying its position as the primary venue for stablecoin arbitrage and large-volume trades.

Osmosis

Osmosis has introduced a generalized StableSwap model that extends the algorithm beyond simple pegged assets to include semi-correlated pairs. This flexibility allows for more diverse liquidity pools while maintaining the low-slippage benefits essential for stablecoin trading. The protocol’s modular design enables developers to customize pool parameters, offering a robust alternative for users seeking exposure to correlated assets without the high costs of constant product models.

Balancer

Balancer integrates StableSwap into its flexible pool architecture, allowing users to create weighted pools that include stablecoin components. This hybrid approach enables sophisticated liquidity strategies, such as combining volatile assets with stablecoins in a single pool. While not as specialized as Curve, Balancer’s versatility makes it a strong option for users who want to diversify their liquidity provision across different asset types within a single protocol.

When to use traditional AMMs

StableSwap’s low-slippage design is a specialized tool, not a universal replacement for constant product AMMs. Traditional automated market makers remain the superior choice for volatile, non-correlated asset pairs where accurate price discovery is essential.

The fundamental tradeoff lies in how the algorithm handles price sensitivity. StableSwap prioritizes capital efficiency for pegged assets by flattening the curve near the peg. However, this design introduces significant impermanent loss risk when dealing with assets that diverge in value. For pairs like ETH/USDC or BTC/ETH, the constant product formula ($x \times y = k$) provides a more balanced risk profile, allowing the pool to adjust prices more naturally in response to market volatility.

Use traditional AMMs when trading assets with independent price movements. In these scenarios, the higher slippage is a feature, not a bug, as it reflects the true market price and prevents arbitrageurs from exploiting a static pricing model. StableSwap is best reserved for stablecoin swaps or highly correlated assets where price stability is the primary goal.

Frequently asked questions about StableSwap

StableSwap is an automated market maker (AMM) algorithm designed specifically for assets that maintain a 1:1 peg, such as stablecoins. Unlike standard constant product models, it offers significantly lower slippage for these pairs, making it the preferred choice for high-volume swaps between similar assets.

How does StableSwap differ from Constant Product AMMs?

The primary difference lies in how they handle liquidity concentration. Constant Product AMMs use a flat curve that results in high slippage for small price changes, which is inefficient for pegged assets. StableSwap introduces a hybrid curve that behaves like a Constant Sum AMM near the peg, providing near-zero slippage for small trades. As it moves away from the peg, it transitions to a Constant Product curve to prevent large price impacts. This design effectively concentrates liquidity around the 1:1 range, improving capital efficiency for traders.

What are the main risks of using StableSwap pools?

While efficient, StableSwap pools are not without risk. The most significant danger is "de-pegging," where one asset loses its 1:1 value relative to the other. If a stablecoin de-pegs, the pool will absorb the losing asset, potentially leaving liquidity providers with a significant loss. Additionally, these pools are vulnerable to arbitrage attacks if the external market price diverges significantly from the pool price, though the curve design mitigates this compared to simpler models.

Can I use StableSwap for volatile assets?

StableSwap is generally not recommended for highly volatile assets like major cryptocurrencies. The algorithm is optimized for assets with low volatility and a tight peg. Using it for volatile pairs can lead to poor pricing and increased impermanent loss for liquidity providers. For volatile assets, a standard Constant Product AMM or a concentrated liquidity model is typically more appropriate and efficient.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!