How StableSwap Curves Reduce Slippage

Use this section to make the StableSwap Protocol vs Standard AMMs decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Comparing Fees and Liquidity Depth

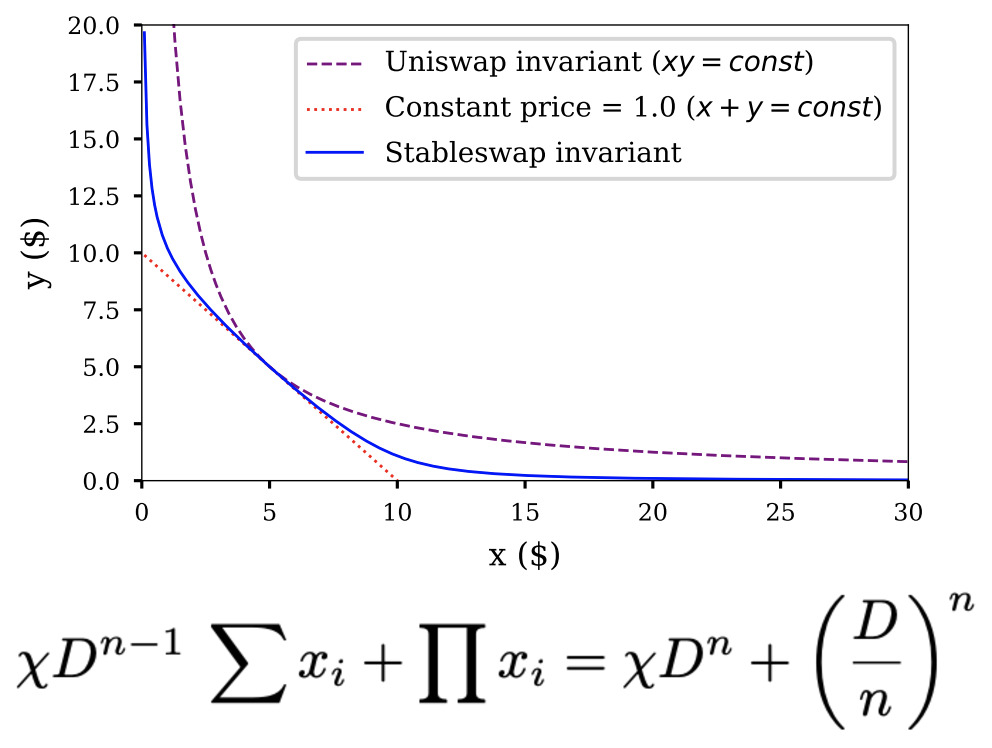

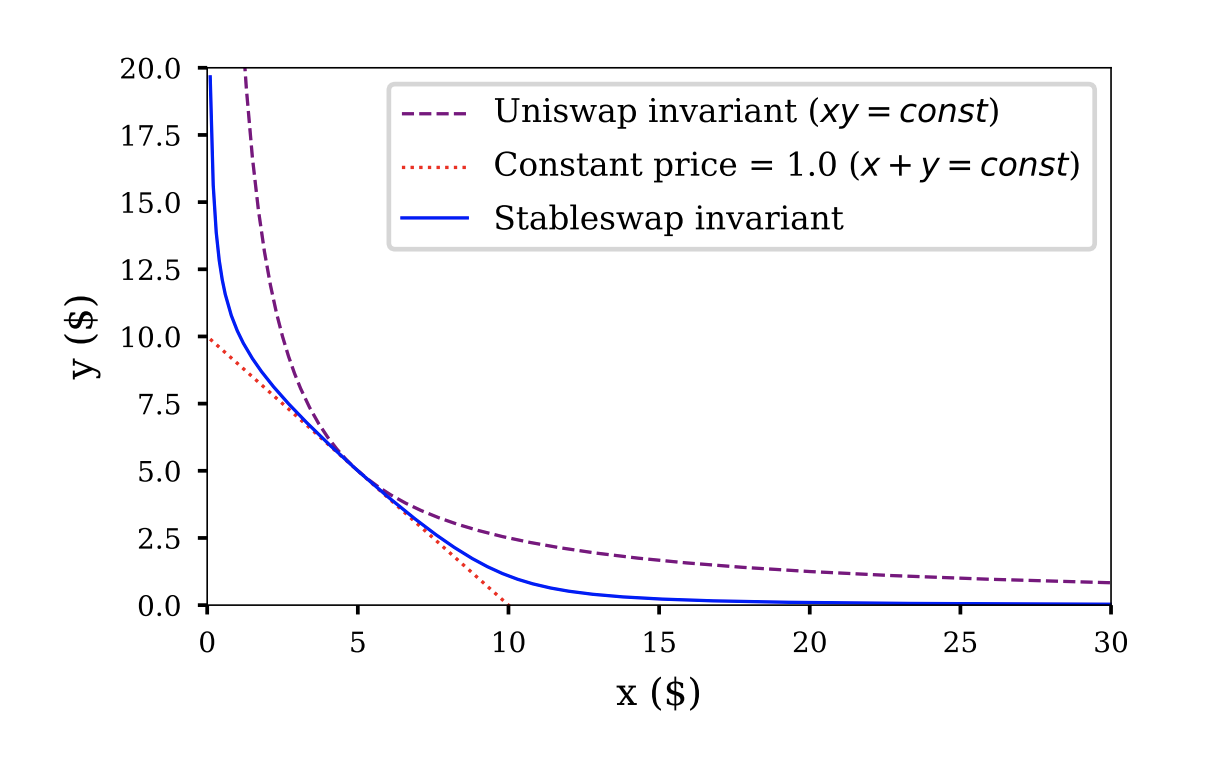

When trading stablecoins, the difference between a standard Automated Market Maker (AMM) and a StableSwap protocol is not just a matter of convenience—it is a matter of capital efficiency. Standard AMMs rely on the constant product formula ($x * y = k$), which creates significant price impact (slippage) as trade size increases relative to pool depth. StableSwap protocols, pioneered by Curve Finance, utilize a hybrid invariant curve that behaves like a constant product for small trades but transitions to a constant sum mechanism for larger trades. This mathematical adjustment keeps the price stable near the peg, drastically reducing slippage for institutional-sized orders.

Fee Structures

Fee structures differ fundamentally in how they capture value and incentivize liquidity providers. Standard AMMs typically charge a flat fee (often 0.3%) on all trades, regardless of asset volatility. This fee is necessary to compensate LPs for impermanent loss and price risk. In contrast, StableSwap protocols charge significantly lower fees (often 0.04% or less) because the assets being traded are pegged to the same value (e.g., USDC to USDT), eliminating impermanent loss risk. The lower fee structure is sustainable because the protocol relies on high volume and the stability of the peg rather than volatility premiums.

Effective Liquidity and Slippage

Liquidity depth in StableSwap is optimized for large trades. In a standard AMM, a $1 million trade against a $10 million pool might result in 5-10% slippage. In a StableSwap pool with similar depth, the same trade might incur less than 0.1% slippage. This is critical for institutional execution, where large orders must be filled without moving the market price against the trader. The protocol’s ability to maintain a tight peg ensures that large swaps do not disrupt the underlying asset’s value.

| Feature | Standard AMM | StableSwap Protocol |

|---|---|---|

| Primary Use Case | High-volatility pairs | Stablecoin pairs |

| Typical Fee | 0.30% | 0.04% |

| Slippage on $1M Trade | High (5-10%+) | Low (<0.1%) |

| Impermanent Loss Risk | High | Negligible |

| Best For | Retail traders | Institutional orders |

For traders executing large stablecoin swaps, the choice between these mechanisms directly impacts the bottom line. Standard AMMs are designed for price discovery in volatile markets, while StableSwap protocols are engineered for efficient settlement. Understanding this distinction is essential for anyone prioritizing low slippage and cost-effective trading in 2026.

When to Use StableSwap vs General AMMs

Choosing between StableSwap and general Automated Market Makers (AMMs) depends entirely on the volatility of the assets you are trading. StableSwap protocols, pioneered by Curve Finance, are engineered for a specific niche: swapping assets that maintain a pegged value. General AMMs, like Uniswap, are built for price discovery in volatile markets. Using the wrong tool for the job results in excessive slippage and unnecessary fees.

Ideal Use Cases for StableSwap

StableSwap excels when trading assets with a stable price relationship, such as fiat-pegged stablecoins (USDC, USDT, DAI) or liquid staking tokens (stkBNB, BNBx). Because the invariant curve is optimized for near-zero volatility, trades execute with minimal slippage even for large volumes. This makes StableSwap the preferred choice for arbitrageurs, yield farmers moving liquidity between protocols, and users rebalancing stable portfolios.

For example, swapping USDC for USDT on a general AMM might incur significant fees due to the standard constant product formula. On a StableSwap pool, the same trade is nearly free, preserving capital efficiency. PancakeSwap’s implementation of StableSwap specifically targets these low-volatility pairs to offer lower slippage than standard AMMs for assets priced closely together.

When General AMMs Are Necessary

General AMMs are essential for trading volatile assets, such as ETH, BTC, or emerging altcoins. These assets experience wide price fluctuations, requiring an AMM design that can handle large price deviations without breaking the pool. StableSwap’s invariant curve cannot accommodate this volatility; attempting to use it for volatile pairs would result in immediate impermanent loss or pool insolvency.

Also, general AMMs support exotic pairs and assets without a stable peg. If you are trading a new token against ETH, or a meme coin against a stablecoin, a standard AMM is the only viable option. The constant product formula ($x * y = k$) allows the price to adjust dynamically to market demand, ensuring liquidity remains available even as the asset’s value swings wildly.

Decision Framework

The decision is binary: use StableSwap for stability, and general AMMs for volatility. If your assets are pegged or highly correlated, StableSwap offers superior capital efficiency. If your assets are volatile or uncorrelated, general AMMs provide the necessary flexibility and price discovery mechanisms. Always verify the pool type before swapping to avoid paying premium fees for a suboptimal trade path.

Institutional Adoption and Risk Factors

As institutional capital moves into decentralized finance, the margin for error shrinks to near zero. Standard Automated Market Makers (AMMs) often struggle with the high-volume, low-volatility trading patterns that institutions require, leading to unacceptable slippage and execution costs. This is where StableSwap Protocol mechanisms distinguish themselves, offering the precision needed for large-scale deployments.

However, the specialized nature of StableSwap introduces distinct risk vectors. While protocols like PancakeSwap’s StableSwap feature are designed to trade stable pairs with lower slippage based on invariant curve functions, they are not immune to smart contract vulnerabilities. The complexity of the bonding curve formulas, originally developed by Curve Finance, requires rigorous verification. Institutions must treat audit reports as primary due diligence, not optional reading.

Impermanent loss mitigation is another critical factor. Standard AMMs penalize liquidity providers when asset prices diverge significantly. StableSwap’s invariant curve is engineered to keep assets pegged closely together, such as USD stablecoins or liquid staking tokens, thereby reducing the drag on capital efficiency. This stability makes it a preferred vehicle for treasury management and yield strategies where capital preservation is paramount.

The decision to adopt StableSwap over standard AMMs ultimately hinges on risk tolerance and volume. For high-frequency or large-capacity trades involving stable assets, the reduced slippage justifies the additional smart contract risk profile. For smaller, sporadic trades, the simplicity of standard AMMs may suffice. Institutions must weigh the operational efficiency of StableSwap against the need for battle-tested, audited security.

Frequently asked: what to check next

What is StableSwap?

StableSwap is an automated market maker (AMM) variant designed specifically for assets with similar values, such as stablecoins or wrapped Bitcoin. Unlike standard AMMs that use a constant product formula, StableSwap employs an invariant curve that reduces slippage for these pairs. This allows traders to swap assets like USDT, USDC, or BUSD with minimal price impact, making it the preferred mechanism for high-volume stablecoin trading in 2026. For implementation details, refer to the PancakeSwap StableSwap documentation.

Why does StableSwap have lower slippage than standard AMMs?

Standard AMMs increase slippage exponentially as the ratio between two assets deviates from a 1:1 balance. StableSwap solves this by using a hybrid invariant that behaves like a bonding curve when balances are equal and transitions to a constant product model only when imbalances become significant. This mathematical adjustment ensures that large trades between similarly priced assets execute at rates closer to the mid-market price, preserving capital efficiency for traders.

Can I use StableSwap for volatile assets like ETH or BTC?

StableSwap is optimized for assets that maintain a peg or narrow price correlation. While some protocols allow volatile assets, the slippage benefits diminish rapidly if the assets diverge in value. For trading volatile pairs, standard AMMs or concentrated liquidity pools are generally more efficient. Use StableSwap primarily for stablecoin swaps, liquid staking derivatives, or wrapped assets that track a single underlying peg.

No comments yet. Be the first to share your thoughts!